So you want to build an emergency fund but your aren’t sure where to start. You may be asking, how is an emergency fund different from my savings account? How much should I be saving? Where should I put the money I save? These are all excellent questions that we will address in this article.

How is an emergency fund different than a savings account?

While an emergency fund and a savings account both entail saving money, they serve very different purposes. An emergency fund is a savings account, but a savings account is not always an emergency fund. For example, when you want to buy something, you can dip into your savings account (money you already have, not credit) to purchase the item. It can be used to purchase anything you want whenever you want without going into debt for that item. This account can be very fluid. You consistently save money into this account, but you also pull money out of it and into your checking account to spend.

Meanwhile, an emergency fund is a lump sum of money you only use to help pay for emergencies. You do not use this money for any other purpose, end of story. It is essentially off-limits except in dire circumstances. An emergency fund is meant to insure you against risk, not fund a buying spree. The key to making sure your emergency fund does not turn into just another savings account is to create a list of criteria under which you can use this account. For example, your car dies and you need to either fix the vehicle or replace it entirely. Losing your car would affect your ability to get to work and earn money so it would absolutely fall into the emergency category. An example of how “not” to use this fund is finding out your friends are going on a trip to Hawaii and you want to join. While this is something you want to do, it is not an emergency and should come from a regular saving account leaving your emergency fund untouched.

Why should I build an emergency fund?

First things first, let’s cover why building an emergency fund is one of the best financial decisions you can make. Life is unpredictable. One day you are flying high and the next you are on the side of the road with a flat tire. An emergency fund is your safety net or rainy-day fund for when unexpected expenses hit you sideways. Your emergency savings can help you weather storms like job loss, medical expenses, home-appliance repairs, major car fixes, accidents, and more.

When troubles come, they can leave you anxious and scared. Emergency funds are easily accessible and designed to give you peace of mind. They prevent you from needing to use credit cards and shoulder unwanted debt. These funds help you rest easy knowing that whatever comes your personal finances are secure.

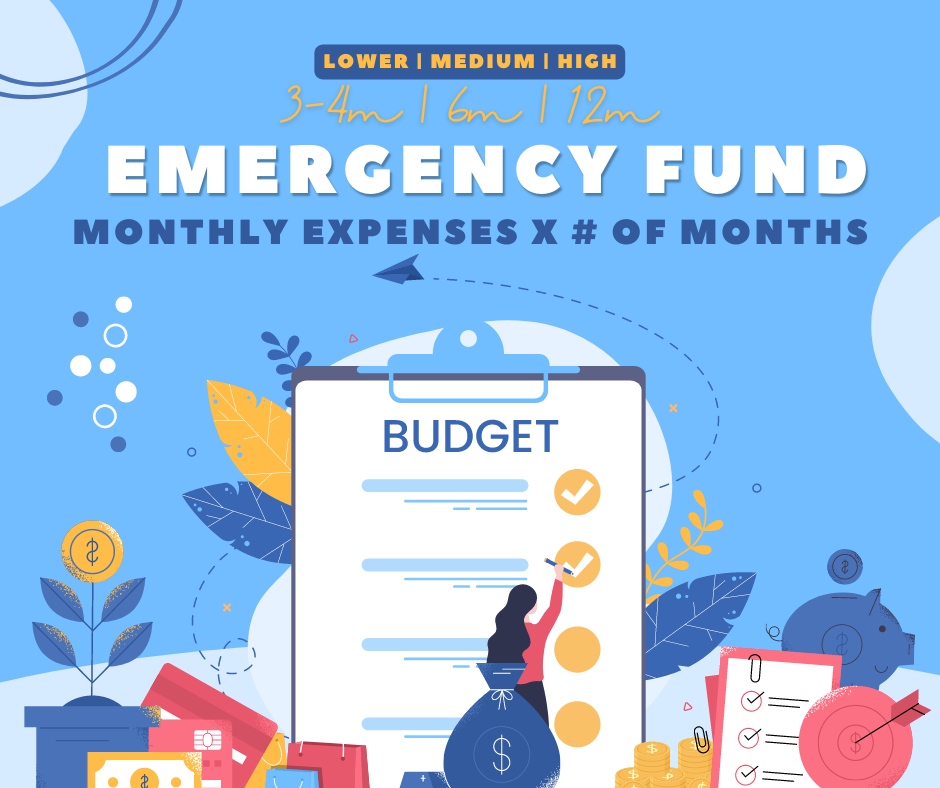

How much should I have in an emergency fund?

When it comes to saving the right amount of money for you and your family, and good rule of thumb is three to six months of living expenses. Experts suggest this much because it is typically a larger amount that can, by nature, help with big unexpected events. However, you will be the best person to make your financial planning decisions. There are a few different routes you can take depending on where you find yourself in life.

Why to save a lower amount: 3-4 Months

There are good reasons to have a smaller emergency fund, specifically only three to four months of living expenses. If you are young and healthy with low debt, low cost of living, a reliable job and vehicle, a strong support network and no dependents, you can get away with less. Operating a lean emergency fund may allow you to pay off other debts or keep money liquid for other investments like a mutual fund.

Why to save a medium amount: 6 Months

Similarly, there are reasons to save six month of living expenses. For example, if you have a high cost of living, lower job security, own your home, support multiple dependents, have a medical condition or a weak support network you may want to build a larger emergency fund. Essentially, if there is more that could go wrong, you will want more money to keep you secure.

Why to save a high amount: 1 Year

Finally, there are those who will want to save a year’s worth of living expenses. These people earn a high income but work in a niche job that would be hard to replace. They are the sole provider to multiple dependents and may be looking to retire soon. The goal, as always is to protect yourself from worst-case scenarios.

How do I calculate how much to put in my emergency fund?

So you know which category you fit in and want to start saving, but how much to save? This is a good time to take a look at your monthly or even weekly budget. A good rule of thumb is to calculate one month’s work of living expenses. Then you will multiply that amount by the number of months you have chosen. That amount is what you should have in your emergency fund.

Where should I keep my emergency savings?

Now that you have identified how much you need to save, where you save that money is important. Society is way past hiding cash under a mattress. After all, if your house burns down, that emergency fund is going right with it as well as your savings efforts. Experts recommend setting up a high yield savings account that is connected to your checking account.

A high yield saving account has a high interest rate. Money market accounts can be great high yield savings accounts to use. Setting up this kind of bank account is a great way your money can begin making you money. By connecting the savings account to your checking account you will have quick access to it if(and only if) an emergency should arise.

How do I build my emergency savings?

Now comes the exciting part, you get to start building your emergency fund. Saving money can come in all methods and sizes. Some individuals will adjust their budget to help them save more for this purpose. Others will stow away a tax refund, work a side hustle, sell items, stop dining out, or skip a shopping trip until they hit their goal.

The key is to make a savings goal and prioritize it in the long term. Depending on how big your emergency fund should be your goal could be short term. Wither way, when you hit your goal, celebrate in free ways. Above all else, enjoy watching the money roll in knowing that you are making an investment in not only your financial goals, but your financial security.